Global smartphone production jumps 12%

EP&T Magazine

Electronics Wireless Apple consumer Electronics smartphones wirelessGlobal brands ramp up production targets - Apple leads the way

TrendForce’s latest insights reveal a significant rebound in global smartphone production, marking the end of an eight-quarter slump in 3Q23. In a strategic year-end surge, brands amped up production to capture more market share, propelling Q4 smartphone output up 12.1% to reach 337 million units. Despite this impressive final quarterly growth, 2023 rounded off with a slight 2.1% dip in annual production—totaling 1.166 billion units.

The outlook for 2024 hints at a brighter future, free from the inventory pressures of the previous year. However, the pace of market recovery remains under scrutiny. The spotlight is on AI applications, with industry giants joining forces to usher in the next wave of AI-powered smartphones.

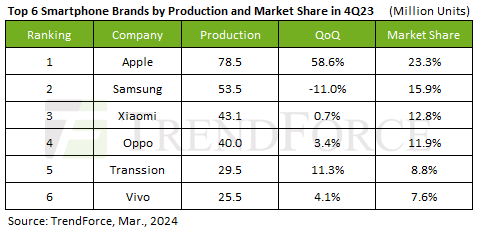

Brands ramp up production targets

Apple stole the show in Q4 with a staggering 58.6% production surge—thanks to the buzz around its iPhone 15 series—cementing its lead with roughly 78.5 million units produced. However, despite leading the pack, Apple experienced a 4.2% decline in annual production, dropping to 223 million units and securing second place. With Huawei’s resurgence, Apple is anticipated to encounter heightened competition in China’s premium market segment, where both brands vie for the same high-end consumer base.

Samsung navigated through a transitional phase in Q4, seeing an 11% decline in production to about 53.5 million units, yet still holding firm at second place for the quarter. Meanwhile, its yearly production took an 11.3% hit, slipping to 229 million units and narrowing its lead over Apple to a mere 0.5%.

Xiaomi (including Xiaomi, Redmi, and POCO) slightly grew its Q4 production by 0.7%, reaching 43.1 million units and maintaining its third position despite a 6.1% annual decrease to 147 million units. Oppo (including Oppo, Realme, and OnePlus) followed closely with a 3.4% quarterly increase, rounding off the year with a 4.1% dip to 139 million units. Vivo (including Vivo and iQoo) managed a 4.1% growth in Q4, ending the year on a 2.9% decrease with 93.5 million units and sliding to sixth place in global production. Smartphone brands with a significant stake in the Chinese market are bracing for heightened competition amid a downturn in China’s consumer spending and Huawei’s aggressive market return.

Transsion expands presence in India & South America

A standout performer, Transsion, (including TECNO, Infinix, and itel) not only achieved a robust 11.3% growth in Q4 but also made history by breaking the 90 million annual production barrier—marking a 46.3% YoY increase. This propelled Transsion to the fifth spot globally, which TrendForce attributes to the replenishment of channel inventory, moving beyond entry-level products to more diverse offerings, and successful expansion into new markets such as India and South America.

TrendForce’s Department of Semiconductor Research.