Additive manufacturing: A dynamic and innovative industry

By Sona Dadhania, technology analyst, IDTechEx Cambridge, UK

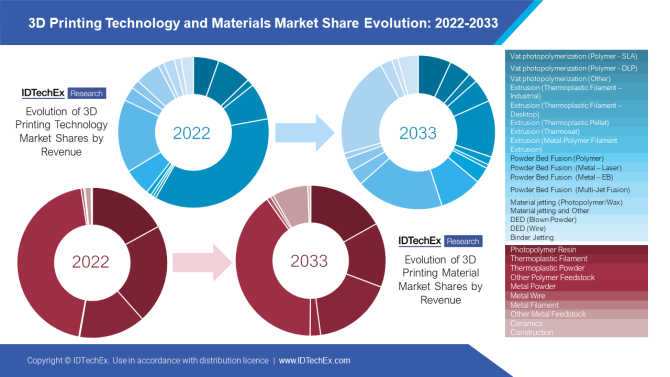

Electronics Production / Materials Supply Chain 3D materials productionSet to surpass US$41 billion by 2033, says IDTechEx

Since the invention of the first 3D printing technologies in the early 1980s, the 3D printing market has experienced a tremendous amount of innovation and interest. A niche technology until the expiration of key patents, the 2010s allowed many start-ups to emerge offering inexpensive consumer-level 3D printers.

The subsequent media frenzy in the early 2010s thrust 3D printing into the limelight, accompanied by major multinational corporations like HP and GE entering the 3D printing space. After years of hype, the industry has moved on to a more critical examination of the value-add that additive manufacturing brings to businesses and supply chains. Despite the obstacles posed by the COVID-19 pandemic and persistent supply chain disruptions, the additive manufacturing market continues to find new applications and end-users.

IDTechEx forecasts that 3D printing’s continued innovation and meaningful adoption will lead the hardware and consumables market to surpass US$41 billion by 2033.

IDTechEx has studied the 3D printing industry for over a decade and has released their latest report providing the most comprehensive view of the market. In examining thirty individual 3D printing technologies and five major material categories, IDTechEx finds a continuous theme between these important aspects of the industry: expansion.

Expanding through new technologies, players

Given that established additive manufacturing technologies like selective laser sintering and thermoplastic filament extrusion are decades old, it might be expected for the market to consolidate and stabilize from a technology standpoint. However, new entrants with their own unique innovations on 3D printing are popping up every year, some of which are so unique that they don’t fit into the classic seven printing processes framework. New technologies, which span polymer, metal, electronics, ceramics, construction, and composite 3D printing, offer different advantages and disadvantages to incumbents. Parallel to these new technologies are more incremental improvements in established processes. What both advancements allow is access to new applications and end-users that 3D printing previously struggled to reach.

3D printing ecosystem: materials, software, post-processing, services

Taking place in tandem with the expansion and improvement of the 3D printing hardware portfolio is the growth of the broader 3D printing ecosystem, including materials, post-processing, software, and services. For example, the 3D printing materials portfolio is expanding because of the aforementioned new technologies entering the market, which can process materials previously underused or underutilized by additive manufacturing. In addition, the software, scanners, and services sector of 3D printing is introducing new offerings to simplify the adoption of additive manufacturing by end-users, making their experience more seamless.

————————

Click here for more information on this report.