OEM semiconductor design spending to hit historic high

By Myson Robles-Bruce, research manager, semiconductor value chain, IHS Markit

Electronics Semiconductors Supply Chain semiconductors semiconductorsBreak through on $300 billion ceiling achieved as robust demand continues unabated

By the time the year is over, the world’s top industrial and electronics manufacturers will have spent more than $300 billion on semiconductors, a threshold being crossed for the first time as robust demand continues unabated in the seven major markets where chips are continually used and needed.

Semiconductor design spend for the served available market (SAM) is projected to reach $316.8 billion this year, a new record that will shatter the previous high mark set last year when the SAM for chip-design spending shot up to $296.8 billion. The findings are contained in a recent IHS Markit report that analyzes the expenditures being made on semiconductor design at any given point in time. With a dollar value assigned to how much is spent on semiconductors by an entity for the products it manufactures or commissions to be made, the “design influence” or “design spend” of a company, country, or geographic regional market can be determined.

The design-spend SAM in 2018 will remain strong, thanks to expensive memory components whose high prices carried over to this year after puffing up the chip market in 2017. Last year’s boom gave memory companies surplus cash to increase investment in production capacity and to boost output, improving the supply of NAND and DRAM and forcing prices to soften. But the days of costly memory chips may be coming to an end, as supply-and-demand dynamics are showing signs of stabilizing this year. Also contributing to overall growth in design-spend SAM this year is the strong performance of markets like automotive and industrial, in which semiconductor content has been traditionally lower, as applications in both arenas become more digitalized and connected.

The winners: a vaunted circle with plenty of cash—and influence—to spare

Among the world’s regions, Asia Pacific will exert the greatest influence on semiconductor procurement decisions, claiming approximately 46% design spend share. With the rise of South Korean and Chinese OEMs in the global market, a considerable portion of chip design spending has moved to Asia Pacific from other regions.

The United States will continue to command the largest share of design spend among countries. However, its projected share of nearly 28% by year-end is down from last year’s 29%, as spending on the wireless sector weakens because of the slowing sales of premium smartphones and media tablets in a market close to saturation. Even so, design spend in the United States will grow 4% in 2018 to more than $88 billion, driven by vigorous chip spending in the industrial and computing markets. Close behind the United States in second place is China/Hong Kong with 25% share of the global total, or 56% of Asia Pacific’s overall spending.

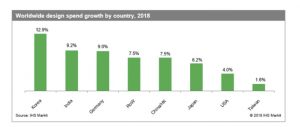

The largest growth will be delivered by South Korea, up 13% this year to $29 billion from a year ago, owing to heightened spending by two of the country’s biggest conglomerates, Samsung and LG Electronics. Two other fast-growing territories are India and Germany, both posting increases in chip-design spending of 9% or more, as shown in the chart below.

The seven markets, at a glance

Of the seven major markets for chip-design spending, the largest share this year of OEM design-spend SAM will be in wireless communications. Though still controlling a hefty 36.7% share, wireless will be down a slight 0.4% from 2017, impacted by plateauing demand for smartphones and media tablets. In second place after wireless is computer platforms, where design spend is flourishing because of renewed interest in both consumer and enterprise computing, driven by new form factors, operating systems, applications, and cloud and storage requirements. In third spot is industrial, supported by solid spending growth across all industrial submarkets as demand improves for industrial machinery and equipment, and as new Internet-of-Things connectivity and computing technologies are adopted at scale.

In fourth place is automotive, currently undergoing rapid transformation as novel features powered by semiconductor are increasingly integrated into vehicles. In fifth spot is the consumer sphere, spurred by increased spending from high-design-spend submarkets such as TVs and consumer appliances, as well as from emerging applications including smartwatches and other wearable electronics. Even so, consumer’s share has contracted over the years given the widespread adoption of smartphones, which has cannibalized the sales of digital cameras, digital media players, video game consoles, and even TVs.

Myson Robles-Bruce, research manager, semiconductor value chain, IHS Markit

In sixth position is computer peripherals, buoyed by strong demand for storage products and high memory pricing. However, demand for some of its applications—such as smart cards, monitors, projectors, and printers—has been in decline. In seventh—and last—place is wired communications, where demand is growing for small-office/home-office and enterprise communications equipment.