Industry outlook remains strong even as headwinds mount

By Shawn G. DuBravac, PhD, CFA - IPC chief economist

cable Editor Pick harnesses wireRussia-Ukraine war adds pressure to harness industry

Each month, IPC publishes a report examining the current sentiment of the wire harness and cable assembly industry and the expectations for the months ahead. In the last month, the outlook has dimmed slightly. This has been driven by numerous forces, including the Russian invasion of Ukraine.

The attack and subsequent trade sanctions has put pressure on already strained supply chains. The offensive also put upward pressure on prices which further exacerbates the challenges faced by the industry. But despite these new challenges compounding existing challenges, the outlook remains strong. Order flow continues to be strong and backlogs are robust, suggesting the outlook for demand remains strong even as headwinds mount.

Russia launched a full-scale invasion of Ukraine on February 24, 2022. In the ensuing weeks, the industry has begun to feel pressures brought on by this war. While the United States does not trade extensively with Russia, Russia and Ukraine are both large producers and exporters of numerous commodities. Global sanctions have put upward pressure on the prices of diverse resources. In some cases, primarily where Russia is a key global supplier, sanctions have also put pressure on the availability of key inputs.

Source: IPC

Roughly four-fifths of wire harness manufacturers expect the war to have a negative impact on transportation costs, while three-fourths expect it to negatively impact commodity prices and three-fifths anticipate a negative impact on the stock of raw materials. Notably, most wire harness and cable assembly manufacturers are anticipating no change to demand for the things their company produces as a result of the Russia-Ukraine conflict when compared to the rest of the electronics manufacturing supply chain, who are instead more likely anticipating a negative impact to their business. Manufacturers expect the automotive, consumer, and industrial electronics markets to be most negatively Impacted by conflict, while anticipating the defense market to be positively impacted

Costs up across the board

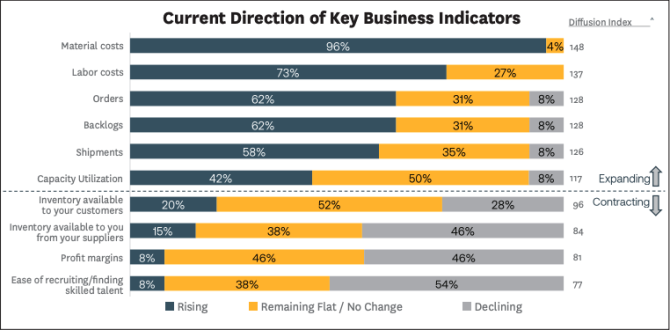

The wire harness and cable assembly industry is feeling the pressure of higher prices and expects prices to continue to rise in the coming months. In April, the Material Costs Index for the industry rose to 148, matching its highest level. Wire harness manufacturers are nearly uniformly in agreement that material costs are up. While the vast majority expect prices to rise further over the next 6 months, the Material Costs Outlook Index did decline slightly over the last month.

Inventories remain constrained

Supply chain challenges remain acute. Inventories available to customers (our IAC Index) slipped into contractionary territory this month, suggesting inventory levels remain low. While executives expect this to improve over the outlook horizon, the outlook has dimmed somewhat in the last month.

Executives also report that inventories available to them from their suppliers (our IAFS Index) improved marginally but remains in contractionary territory. This suggests the majority of respondents are experiencing inventory constraints. At the same time, the outlook for this indicator improved over the last month. Executives expect inventory available for suppliers to improve over the next six months.

Demand remains strong

Industry demand remains robust despite higher prices, growing uncertainties, and continued supply chain challenges. The New Orders Index declined in the last month but remains well in expansionary territory. The outlook has weakened, but the majority of respondents expect demand to remain strong in the months ahead. Moreover, backlog orders remain high and executives expect them to remain high for at least the next six months. The strong backlog in orders provides some cushion should demand slow. It will provide wire harness manufacturers more time to adjust to slowing demand.

While most headlines are focused on the implication of the war on economic growth, it is not the only risk we should be worried about. Another key risk to the economy is the impact high inflation rates are having. Last month the Federal Reserve initiated its first-rate hike. The Fed also signaled six more rate increases are coming by the end of the year. These increases will bring the target fed funds rate to nearly 2%. Furthermore, another 3 to 4 rate increases are expected in 2023 which will push the target fed funds rate to just under 3%. Higher rates will slow demand which in turn will hopefully ease supply chain constraints and other supply chain dislocations. The Federal Reserve has set a very hawkish tone. With strong job growth and low unemployment, the Fed will be able to focus almost exclusively on battling inflation over the next 18 months. The European Central Bank (ECB) had also said a hawkish tone but it is now unclear how severe the spillover from the Russia-Ukraine war will be on economic growth in Europe. As a result, the ECB will have to be more tepid with rate hikes in the coming year.

There is some risk that the Federal Reserve will overshoot monetary tightening. Monetary policy works with a lag but given the current high rate of inflation, the Fed may not have the luxury of waiting for the full transmission of rate hikes to work their way through the economy. The Fed will have to watch closely the rate of the economic slowdown that takes place over the next year outside of any slowdown produced by restrictive monetary policy measures.

There are numerous risks exerting influence on the wire harness and cable assembly industry and how executives see the following months unfolding. But overall, the industry remains optimistic about the near-term outlook.

————————

For more information on IPC’s monthly global sentiment report for the wire harness and cable industry, please contact at ShawnDuBravac@ipc.org.