Automotive semis to hit $84B by 2028

EP&T Magazine

Electronics Semiconductors Supply Chain automotive semiconductors supply ChainSemiconductor devices achieve new heights through the transformation of the supply chain: Yole

The semiconductor chip market is expected to see robust growth, increasing from US$43 billion in 2022 to US$84.3 billion in 2028, with an impressive 11.9% CAGR during the period, according to Eric Mounier, Ph.D., director of market research at Yole Intelligence.

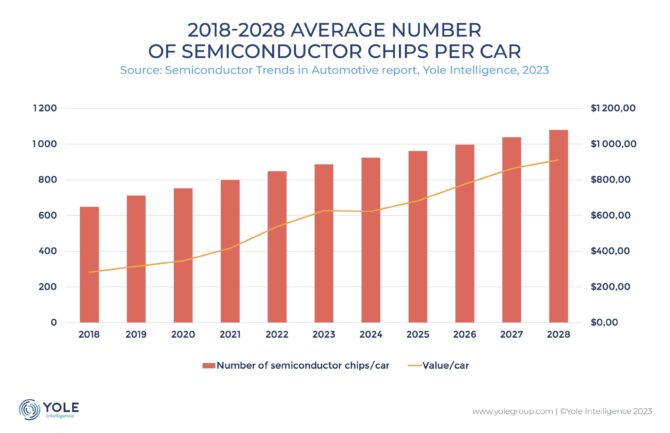

“In 2022, each car contains around US$540 worth of semiconductor chips, which is projected to rise to about US$912 by 2028. This is driven by the adoption of ADAS and electrification, increasing the number of chips per vehicle from 850 to 1,080,” Mounier said.

Key drivers are numerous and include electrification, requiring new substrates like SiC, advanced technology nodes as small as 16nm/10nm for ADAS components and a growing demand for memory, especially DRAM and computing power for Level 4 and 5 autonomous vehicles. At the wafer level, Yole Intelligence reported that wafer shipments to increase from 37.4 million units in 2022 to 50.5 million in 2028. It includes memory, processors, and MCU s leading the way for 12-inch wafers. SiC devices will continue to grow due to EV /HEV adoption, while advanced nodes below 16nm will be driven by ADAS technology. OEMs are increasingly embracing vertical integration to electrify their operations, with strategies varying by industry segment and region. Power electronics and semiconductors are vital focuses, with some OEMs making direct investments.

Although after the COVID linked chip shortage, the focuses of automotive OEMs to semiconductor keep increasing, we see in general a lack of comprehensive strategies on semiconductor among OEMs. For the first time, Yole Intelligence build an analytical model dedicated to automotive semiconductors. The so called ‘Yole Triple-C Model’ is designed to help OEMs in Car, Chip, and Confine metrics, representing respectively the coverage of semiconductor technologies, the depth of involvement in semiconductor value chain, and the resilience of semiconductor supply chain.

Passenger and light commercial vehicles are shifting into a “Market-driven” phase of innovation adoption, while medium and heavy-duty commercial vehicles are starting their electrification journey, primarily due to incentives and regulations.

Key trends in powertrain and electrification include:

- Integration of high-voltage systems.

- Adoption of 800V technology for fast charging.

- The introduction of SiC in supply chains.

- The increasing popularity of dedicated BEV platforms.

ESG concerns are also growing in importance. Si IGBTs are gaining traction to address cost barriers, especially in hybrid solutions with SiC MOSFETs.